EP0138320A2 - Cryptographic key management system - Google Patents

Cryptographic key management system Download PDFInfo

- Publication number

- EP0138320A2 EP0138320A2 EP84305480A EP84305480A EP0138320A2 EP 0138320 A2 EP0138320 A2 EP 0138320A2 EP 84305480 A EP84305480 A EP 84305480A EP 84305480 A EP84305480 A EP 84305480A EP 0138320 A2 EP0138320 A2 EP 0138320A2

- Authority

- EP

- European Patent Office

- Prior art keywords

- card

- terminal

- issuing

- key

- issuing institution

- Prior art date

- Legal status (The legal status is an assumption and is not a legal conclusion. Google has not performed a legal analysis and makes no representation as to the accuracy of the status listed.)

- Granted

Links

Images

Classifications

-

- G—PHYSICS

- G07—CHECKING-DEVICES

- G07F—COIN-FREED OR LIKE APPARATUS

- G07F19/00—Complete banking systems; Coded card-freed arrangements adapted for dispensing or receiving monies or the like and posting such transactions to existing accounts, e.g. automatic teller machines

- G07F19/20—Automatic teller machines [ATMs]

- G07F19/206—Software aspects at ATMs

-

- G—PHYSICS

- G07—CHECKING-DEVICES

- G07F—COIN-FREED OR LIKE APPARATUS

- G07F7/00—Mechanisms actuated by objects other than coins to free or to actuate vending, hiring, coin or paper currency dispensing or refunding apparatus

- G07F7/08—Mechanisms actuated by objects other than coins to free or to actuate vending, hiring, coin or paper currency dispensing or refunding apparatus by coded identity card or credit card or other personal identification means

- G07F7/10—Mechanisms actuated by objects other than coins to free or to actuate vending, hiring, coin or paper currency dispensing or refunding apparatus by coded identity card or credit card or other personal identification means together with a coded signal, e.g. in the form of personal identification information, like personal identification number [PIN] or biometric data

- G07F7/1016—Devices or methods for securing the PIN and other transaction-data, e.g. by encryption

Definitions

- the subject invention relates to a system for distributing cryptographic keys in an electronic funds transfer (EFT) environment.

- EFT electronic funds transfer

- the key management system is particularly suited to permit off-line verification of transaction cards at authorization terminals.

- Financial transaction cards are commonly used as a replacement for cash. These cards, which can either be credit cards or debit cards, can be used instead of cash to purchase goods or services from a merchant. Many cards can also be utilized to obtain cash or traveller's checks from financial institutions or merchants, including through the use of automatic teller machines (ATM's).

- ATM's automatic teller machines

- transaction card fraud There are many types of transaction card fraud. For, example, criminals have used lost or stolen cards to purchase goods or services. criminals have also duplicated or counterfeited cards using valid account numbers.

- Another approach which overcomes many of the shortcomings of card lists, includes on-line authorization terminals.

- merchants are provided with electronic terminals that are connected to the issuer of the cards, possibly through a central processor.

- information encoded on the card is read into the terminal.

- the terminal communicates this information over transmission lines to a host computer having information on the card holder. If the card is valid and the transaction does not exceed a specified limit, the host computer will return an approval to the merchant.

- One method which the applicant has developed, includes placing a secret, encrypted code on the card to guard against counterfeiting.

- anticounterfeiting check digits are derived by encrypting the personal account number (PAN) associated with the card.

- PAN personal account number

- These cryptographic check digits are encoded onto the magnetic stripe of the card.

- the central processor receives the information on the magnetic stripe, which includes-the PAN and the check digits.

- the transmitted PAN is encrypted in a manner similar to the generation of the cryptographic check digits. If the two results compare favorably, the card can be authorized.

- the counterfeiter merely having a valid personal account number, could not generate valid check digits.

- PIN personal identification numbers

- a particular PIN is assigned to each card holder.

- the PIN may be either selected by the card holder or issued by the financial institution. This approach is utilized today in many banks having automatic teller machines.

- the central host compares the transmitted PIN with the associated PIN stored at the central location. If these numbers match, the card holder is identified as the authorized user of the card.

- the latter approach is effective to reduce the unauthorized use of lost or stolen credit cards.

- One example includes the comparison of at least a portion of a cardholder's PIN, at the terminal.

- a portion of the PIN is encrypted and encoded onto the magnetic stripe of the card.

- the key which is used to encrypt the partial PIN values is supplied to the transaction terminals.

- the encrypted information is read from the magnetic stripe and compared with the PIN entered by the card holder, utilizing the secret key stored at the terminal.

- the partial PIN check can be used to authorize low value transactions. If a higher level transaction needs to be authorized, the remainder of the PIN can be verified through the communication network in an on-line manner.

- the off-line approach can also be adapted for use with the anticounterfeiting scheme outlined above.

- each of the institutions could be provided with their own encrypting key.

- the rest of the institutions in the system could still operate.

- the latter approach would require that each terminal be provided with the encrypting keys of each and every institution. Because of the number of institutions, this approach is deemed unfeasible as a long term solution. Therefore, it would be desirable to provide a key management system which would overcome the shortcomings described above.

- the subject invention provides for a key management approach for use in a system which includes a plurality of issuing institutions and a plurality of transaction terminals.

- the system is intended to facilitate the off-line authorization of a transaction card at a terminal.

- a central host is given the responsibility of managing the keys.

- the issuing institutions are connected by communication lines to the host.

- the terminals are also connected by communication lines to the host.

- some transactions may be authorized in a typical on-line manner utilizing the communication lines.

- the subject system also permits security and fraud analysis to take place in an off-line manner.

- the central host will generate a master encryption key.

- the master key will be supplied to each and every terminal in the system. It is intended that the terminals be designed such that if someone tampered with the terminal, the master key would be erased or destroyed.

- the central host also distributes encrypting keys to each issuing institution. These encrypting keys are derived keys. More particularly, each issuing institution will typically have some form of identification number (i.e. Bank Identification Number, BIN). The encryption key sent to the institution is derived by encrypting the BIN, associated with the bank, under the master key. For the remainder of the specification, the term issuing institution and bank will be used interchangably. It should be understood that the scope of the subject invention includes any institution which issues financial transaction cards.

- BIN Bank Identification Number

- the institution When the institution issues the card, a set of data is placed on the card. Among this data is the institution's identification number (BIN). In accordance with the subject invention, the institution will also place authorization information on the card. As discussed more fully hereinbelow, this authorization information can include anticounterfeiting data, personal identification numbers or even dynamic signature information. In any case the authorization information is placed on the card in encrypted form. Furthermore, the authorization information is encrypted under the secondary key associated with the institution.

- this authorization information can include anticounterfeiting data, personal identification numbers or even dynamic signature information.

- this authorization information is placed on the card in encrypted form. Furthermore, the authorization information is encrypted under the secondary key associated with the institution.

- the secondary key When a card holder initiates a transaction, the information from the card is read by the terminal. In order to authorize the transaction, the secondary key must be derived by the terminal. The secondary key is derived by utilizing the master key stored in the terminal to encrypt the BIN placed on the card. Once the secondary key has been derived, it can be used to permit the analysis of the encrypted authorization information placed on the card.

- the above apprqach solves the shortcomings found in the prior art. More specifically, it permits off-line authorization of transaction cards at a terminal. Furthermore, since each individual issuing institution is provided with unique encrypting keys, the compromise of any single issuer's secondary key will not affect the security of the entire system. From a commercial standpoint, it is necessary to have each individual institution responsible for its own security. This result is achieved with the key management approach of the subject invention. In addition, while each individual bank is given its own unique key, there is no requirement for each terminal to be provided with all of the keys. Rather, the terminal derives the necessary secondary key utilizing the master key supplied by the central host and the bank identification number. Thus, the terminal does not require large storage capacity but only needs to be provided with one secure master key.

- a central host 20 which acts as a network switch, routing information between a plurality of transaction terminals 22 and issuing institutions 24.

- the issuing institutions can be banks or other service organizations which distribute transaction cards, such as credit cards or debit cards. These cards may be used at various merchants or institutions to purchase goods or services or to obtain cash.

- Each merchant is provided with one or more terminals 22.

- a terminal typically includes a reader for receiving information encoded on the magnetic stripe of the card.

- the terminal may include a PIN pad to permit a customer to enter their personal identification number (PIN).

- the terminal will also include an encryption apparatus which may be provided in the main portion of the terminal or separately in the PIN pad. The location of the encryption apparatus will depend on the particular technique being selected.

- Each of the terminals is connected to the host along communication lines 30.

- the host is also connected to the issuers along communications lines 32.

- information about the card holder and the purchase are transmitted from the terminal, along communication lines 30, to the host.

- the central host will make the approval or denial decision.

- the information is routed along lines 32, to the institution which issued the card.

- the authorization decision made by the institution is retransmitted to the merchant along the same communication lines.

- off-line is defined to mean operations which can be performed at the terminal without any communication to the host.

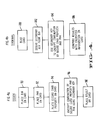

- FIG 2 the general key management system of the subject invention is illustrated. This approach can be utilized to provide both an off-line anticounterfeit check and PIN verification.

- the flow chart is broken into three segments where Figure 2A shows the operations performed at the central host, Figure 2B shows the operations performed by the issuer and Figure 2C shows the actions taken at the terminal.

- the central host or control 20 initially generates a system master key 40.

- This master key is supplied to all of the terminals 42. Since the security of the master key is of utmost importance, this distribution should be handled in a highly secure manner.

- the terminals are physically connected to the host permitting initial loading of the master key. After this time, the terminals are kept under high security until they are installed at merchant locations.

- a key loading device is connected to the host and has the master key loaded therein. The key loading device is then brought to each terminal and physically connected to load the key.

- the terminal should be designed such that any tampering will erase or otherwise destroy the master key, such that it can never be extracted from the terminal.

- the host then generates a plurality of secondary keys 44. These secondary keys are derived utilizing the bank identification number (BIN). As pointed out above, each institution is generally associated with an unique identification number. This identification number is encrypted using the master key. The resulting secondary keys are then distributed to the associated issuers. Again, a number of methods can be used to distribute the keys. Typically, secure encrypted communication lines are already established between the issuers and the host and therefore it is possible to transmit these keys over communication 'lines. The key may also be physically delivered using a key loading device as discussed above.

- BIN bank identification number

- the issuer is now capable of generating transaction cards. Initially, the issuer will place its BIN number on each card 50. Typically, this information is placed on the card by encoding the information on a magnetic stripe. While this approach is fairly common, there many other ways of encoding data on the cards, all of which are within the scope of the subject invention.

- the issuer will then generate authorizaton information 52. As discussed below, this authorization information can be anticounterfeiting digits, PIN information or any other suitable identifier.

- the authorization information is then encrypted, using the secondary key supplied by the host 54.

- the encrypted authorization information is then placed on the card 56 in the manner described above.

- the card can now be authorized in an off-line manner at the terminals.

- the card is initially read by the terminal at 60.

- the terminal will typically have a card reader capable of deciphering the encoded information on the magnetic stripe.

- the terminal should have compatible reading equipment.

- the information which is read includes the BIN number of the institution, as well as the encrypted authorization information.

- the terminal will then derive the secondary key, utilizing the master key stored at the terminal to encrypt the BIN number of the institution 62. Once the secondary key has been derived, it can be used to analyze encrypted authorization information on the card 64.

- the analysis can be handled in a number of ways. The particular approach will depend on the system design and a few examples will be discussed in detail hereinbelow.

- the transaction can be authorized. If the information does not match, the transaction can be denied.

- Figure 3 a more specific approach is shown for use in an anticounterfeiting scheme.

- Figure 3A illustrates the actions taken at the issuer, while Figure 3B describes the events at the terminal.

- Figures 3 through 6 the activities of the central host are identical with those described in, Figure 2 and will not be further discussed.

- the issuer will again place the BIN number on the card 70.

- the issuer will also generate a personal account number (PAN) which is unique for each card.

- PAN personal account number

- This account number or (PAN) is placed on the card 72.

- the issuer will then encrypt the PAN with the secondary key 74.

- the result of this encryption is placed on the card 76. While the above discussion is limited to the use of a PAN, this number may be combined with any other information normally on the card, such as the card expiration date. Further, the entire encrypted information need not be placed on the card but only a subset thereof. By choosing only a specific subset, the information which must fit on the card can be economized.

- the card will be read at the terminal 80.

- both the BIN number and the encrypted PAN information will be received.

- the terminal will then derive the secondary key, utilizing the master key to encrypt the BIN 82.

- the secondary key is then used to encrypt the account number placed on the card at 84.

- the result of this encryption (or at least a portion thereof) can then be compared with the encrypted account information on the card. If these match, the transaction can be authorized.

- the issuer will again place the BIN on the card 90.

- the PAN is also placed on the card 92.

- the secure card property such as the Watermark is placed on the card. Because of the manufacturing sophistication necessary to implant a secure property, this step will typically be initially handled by an entity other than the issuer. The cards with the secured property placed thereon will then be supplied to the issuer. Thus, it is not intended that the order of the placement of the information on the card restrict the scope of the subject invention.

- the secure property which would provide some form of numeric information, is then combined with the account number and encrypted, using a secondary key 96. The result of this encryption is then encoded on the card 98.

- the information on the card including the secure property, is read by the terminal 100.

- the secondary key is derived, utilizing the master key to encrypt the BIN 102.

- the PAN and secure property are combined and are encrypted using the secondary key 104.

- the result of this encryption is then compared with the encrypted information encoded on the card 106. As in the previous cases, if the information matches, the transaction can be approved. However, if the information does not match, the transaction can be denied.

- the use of the key management system is illustrated for use with information particularly associated with the card holder, such as a PIN.

- the identical system can be used for any other information associated with a specific card holder, such as dynamic signature analysis information.

- the handwriting analysis information unique to the cardholder, would be encoded in numeric form and encrypted, using the proper key.

- the remainder of discussion of Figures 5 and 6 will be restricted to the use of PIN's.

- the issuer will once again place its BIN number on the card 110.

- a PIN will then be generated to be associated with the customer.

- the bank generates this PIN.

- the PIN may also be supplied to the issuer by the cardholder.

- the particular approach taken can be left to the discretion of the issuing institution as there are various advantages and disadvantages with both techniques. The benefits of each technique is discussed in detail in a bulletin by the American National Standards Committee (ANSI) publication on Pin Management and Security, ANSI-X9.8 (1982). If the PIN has been generated by the institution, it must be supplied to the cardholder.

- ANSI American National Standards Committee

- the PIN which has been selected is then encrypted using the secondary key 114.

- the result of this "encryption is then placed on the card 116.

- this system is probably best utilized using only a partial PIN value. For example, where four digits constitute the PIN, only two digits are encrypted and placed on the card. The remaining two digits are utilized for higher value, on-line authorization.

- the partial PIN digits may also be derived using the full PIN. All or only a portion of these derived digits may be placed on the card. The details of implementing a partial PIN system are-known in the prior art and need not be discussed in detail.

- the card to be used is read by the terminal 120.

- the secondary key is derived by encrypting the BIN utilizing the master key stored at the terminal 122.

- the card holder will then enter his PIN.

- the PIN may be entered through the PIN pad of the terminal 124.

- the secondary key is then utilized to compare the encrypted PIN information on the card with the PIN entered by the card holder 126. This comparison may be carried out either by encrypting the PIN entered by the card holder or by decrypting the encrypted PIN on the card such that both PINs are in clear text.

- the issuer places the BIN number on the card 130.

- the PAN is placed on the card 132.

- a PIN is generated 134 in a manner described above.

- the PAN is encrypted 136.

- the resulting encryption is then combined with the PIN to define a coded value 138.

- the card is read at the terminal 150.

- the PIN is received from the cardholder 152.

- the secondary key is then derived utilizing the master key to encrypt the BIN 154.

- the PAN is then encrypted under the secondary key 156.

- the encrypted PAN is then compared with the information placed on the card. This can conveniently be done in two ways, as shown at 158 and 160. More specifically, the encrypted PAN (or a portion thereof) is combined with the coded value and then compared with the PIN entered by the card holder. Where the original combination at 138 was by addition, the encrypted PAN is subtracted from the coded value, which should yield the PIN.

- Another alternative (160) is to combine the newly encrypted PAN (or a portion thereof) with the PIN entered by the card holder. This result should generate the coded value which has been placed on the card. In either case, if the comparison matches, the transaction can be authorized.

- a new and improved key management system for use in an EFT environment, which permits off-line authorization of a transaction card.

- a central host generates a master key which is then supplied to all the terminals in the system.

- the host then derives a secondary key for each issuing institution by encrypting the BIN number of the issuing institution under the master key.

- the secondary keys are then supplied to the issuing institution.

- the institution When the institution issues a card, it places its BIN number on the card.

- authorization information is placed on the card in encrypted form. This information is encrypted under the secondary key associated with the institution. This information may include anticounterfeiting digits or PIN information.

- the information on the card is read.

- the terminal then derives the secondary key, utilizing the master key stored at the terminal to encrypt the BIN of the institution.

- the secondary key is then used to permit analysis of the encrypted authorization information which has been placed on the card.

- off-line authorization can be carried out to enhance the security of the transaction card network.

- each of the issuing institutions is given a different cryptographic key, thereby further enhancing overall system security.

- the disclosure has included a description of a number of different security approaches which can utilize the subject key management system. These techniques can be used alone or in combination. If used in combination, it could be beneficial to have the issuing institutions use a different secondary key for each technique. This could be accomplished in a number of ways. For example, a different master key could be generated for each technique, or the BIN could be modified in a set way before it is encrypted.

Abstract

Description

- The subject invention relates to a system for distributing cryptographic keys in an electronic funds transfer (EFT) environment. The key management system is particularly suited to permit off-line verification of transaction cards at authorization terminals.

- In recent years, there has been a clear trend in society to eliminate the use of cash in financial transactions. Financial transaction cards are commonly used as a replacement for cash. These cards, which can either be credit cards or debit cards, can be used instead of cash to purchase goods or services from a merchant. Many cards can also be utilized to obtain cash or traveller's checks from financial institutions or merchants, including through the use of automatic teller machines (ATM's).

- The widespread use of transaction cards has produced a concomittant increase in associated fraud. There are many types of transaction card fraud. For, example, criminals have used lost or stolen cards to purchase goods or services. Criminals have also duplicated or counterfeited cards using valid account numbers.

- A number of systems have been implemented in order to reduce these fraud losses. One approach is to distribute a list of lost or stolen cards to merchants. This list must be checked at the time of purchase to see if a card, which has been presented, is valid. Unfortunately, there are difficulties with this approach. For example, it takes time to distribute the bad card list after the card has been reported lost or stcrlen. Furthermore; card numbers remain on the list for only a certain period of time and when the numbers are removed, active fraud can resume. Finally, it is quite difficult to insure that all clerks in a merchant establishment will religiously refer to the card list.

- Another approach, which overcomes many of the shortcomings of card lists, includes on-line authorization terminals. In this scenario, merchants are provided with electronic terminals that are connected to the issuer of the cards, possibly through a central processor. When a customer presents a card, information encoded on the card is read into the terminal. The terminal communicates this information over transmission lines to a host computer having information on the card holder. If the card is valid and the transaction does not exceed a specified limit, the host computer will return an approval to the merchant.

- While this approach is an improvement over the use of bad card lists, it also has drawbacks. For example, counterfeit cards can be generated with valid account numbers which will not be screened by the system. In addition, because of high communication costs, not all transactions are typically authorized. Thus, a lost or stolen card can often be used in a remote geographical area to purchase goods.

- Because of these latter shortcomings, other systems have been recently proposed to increase security. One method, which the applicant has developed, includes placing a secret, encrypted code on the card to guard against counterfeiting. Preferably, anticounterfeiting check digits are derived by encrypting the personal account number (PAN) associated with the card. These cryptographic check digits are encoded onto the magnetic stripe of the card. When the card is presented to the merchant, the information on the magnetic stripe, which includes-the PAN and the check digits, is read and transmitted to the central processor. At the central processor, the transmitted PAN is encrypted in a manner similar to the generation of the cryptographic check digits. If the two results compare favorably, the card can be authorized. As can be appreciated, without knowledge of the encryption technique used to generate the check digits, the counterfeiter merely having a valid personal account number, could not generate valid check digits.

- Another approach to reducing fraud losses is to require the use of personal identification numbers (PIN's). In this technique, a particular PIN is assigned to each card holder. The PIN may be either selected by the card holder or issued by the financial institution. This approach is utilized today in many banks having automatic teller machines. When a transaction is to take place, the cardholder will enter his PIN into the terminal. The PIN is transmitted, along with the account number on the card, to the central host. The central host compares the transmitted PIN with the associated PIN stored at the central location. If these numbers match, the card holder is identified as the authorized user of the card. The latter approach is effective to reduce the unauthorized use of lost or stolen credit cards.

- The above techniques, however, also have certain shortcomings. These shortcomings are becoming more severe as the geographical reach of the card systems increase. More specifically, both of the above discussed security techniques require that information be transmitted from the merchant to a remote issuer. The communication costs involved in these situations is directly related to the distance between the merchant and the card issuer. Furthermore, as the number of card holders increases, the burdens on computer time also become significant. Therefore, it would be desirable to provide improved security system which can be utilized without having to incur communication costs. This goal can be met through the use of off-line approval techniques.

- There have been some off-line approaches suggested in the prior art. One example includes the comparison of at least a portion of a cardholder's PIN, at the terminal. In this approach, a portion of the PIN is encrypted and encoded onto the magnetic stripe of the card. The key which is used to encrypt the partial PIN values is supplied to the transaction terminals. When the card is used in a transaction, the encrypted information is read from the magnetic stripe and compared with the PIN entered by the card holder, utilizing the secret key stored at the terminal. By this arrangement, a degree of security can be provided without incurring any communication costs. The partial PIN check can be used to authorize low value transactions. If a higher level transaction needs to be authorized, the remainder of the PIN can be verified through the communication network in an on-line manner. The off-line approach can also be adapted for use with the anticounterfeiting scheme outlined above.

- The basic drawback to the off-line approach suggested in the prior art is that there has been no suitable method designed for distributing the encrypting keys throughout the system. Thus, while the latter system can be implemented on a small scale, difficulties arise where there are thousands of transaction terminals and hundreds of institutions issuing cards. Obviously, the simplest answer is to use a single encrypting key for all the institutions, which is then provided to all the terminals. While the keys stored in terminals can be controlled, it is difficult to provide for key security at a large number of issuing institutions. More specifically, terminals can be safely loaded with an encrypting key during manufacture. Furthermore, these terminals can be secured to prevent tampering. However, where a large number of banks are involved, the security of the entire system would be dependent on the security of the weakest link in the group. For example, dishonest employees at one bank could conspire to uncover the key which controls the system. If the key were discovered, the entire off-line system would be compromised. Therefore, in this system, each issuing institution would be forced to rely on the security of all other issuers to guard against fraud.

- To overcome the latter problem, each of the institutions could be provided with their own encrypting key. Thus, if the security at any institution were compromised, the rest of the institutions in the system could still operate. The latter approach, however, would require that each terminal be provided with the encrypting keys of each and every institution. Because of the number of institutions, this approach is deemed unfeasible as a long term solution. Therefore, it would be desirable to provide a key management system which would overcome the shortcomings described above.

- Accordingly, it is an object of the subject invention to provide a new and improved key management "system.

- It is another object of the subject invention to provide a new and improved key management system particularly suited for off-line authorization of a transaction card.

- It is a further object of the subject invention to provide a new and improved key management system particularly suited for the electronics funds transfer environment.

- It is still another object of the subject invention to provide a new and improved key management system permitting the off-line verification of the authenticity of a transaction card at a terminal.

- It is still a further object of the subject invention to provide a new and improved key management system which facilitates the off-line verification of the identity of a card holder utilizing a transaction card at a terminal.

- In accordance with these and many other objects, the subject invention provides for a key management approach for use in a system which includes a plurality of issuing institutions and a plurality of transaction terminals. The system is intended to facilitate the off-line authorization of a transaction card at a terminal. In the subject system, a central host is given the responsibility of managing the keys. Typically, the issuing institutions are connected by communication lines to the host. In addition, the terminals are also connected by communication lines to the host. By this arrangement, some transactions may be authorized in a typical on-line manner utilizing the communication lines. The subject system also permits security and fraud analysis to take place in an off-line manner.

- In accordance with the subject system, the central host will generate a master encryption key. The master key will be supplied to each and every terminal in the system. It is intended that the terminals be designed such that if someone tampered with the terminal, the master key would be erased or destroyed.

- The central host also distributes encrypting keys to each issuing institution. These encrypting keys are derived keys. More particularly, each issuing institution will typically have some form of identification number (i.e. Bank Identification Number, BIN). The encryption key sent to the institution is derived by encrypting the BIN, associated with the bank, under the master key. For the remainder of the specification, the term issuing institution and bank will be used interchangably. It should be understood that the scope of the subject invention includes any institution which issues financial transaction cards.

- When the institution issues the card, a set of data is placed on the card. Among this data is the institution's identification number (BIN). In accordance with the subject invention, the institution will also place authorization information on the card. As discussed more fully hereinbelow, this authorization information can include anticounterfeiting data, personal identification numbers or even dynamic signature information. In any case the authorization information is placed on the card in encrypted form. Furthermore, the authorization information is encrypted under the secondary key associated with the institution.

- When a card holder initiates a transaction, the information from the card is read by the terminal. In order to authorize the transaction, the secondary key must be derived by the terminal. The secondary key is derived by utilizing the master key stored in the terminal to encrypt the BIN placed on the card. Once the secondary key has been derived, it can be used to permit the analysis of the encrypted authorization information placed on the card.

- The methods for analyzing the encrypted information on the card will vary depending on the particular authorization technique implemented. A number of comparison schemes are set forth in the detailed description. It is intended that the scope of the subject invention cover any of these comparisons schemes.

- The above apprqach solves the shortcomings found in the prior art. More specifically, it permits off-line authorization of transaction cards at a terminal. Furthermore, since each individual issuing institution is provided with unique encrypting keys, the compromise of any single issuer's secondary key will not affect the security of the entire system. From a commercial standpoint, it is necessary to have each individual institution responsible for its own security. This result is achieved with the key management approach of the subject invention. In addition, while each individual bank is given its own unique key, there is no requirement for each terminal to be provided with all of the keys. Rather, the terminal derives the necessary secondary key utilizing the master key supplied by the central host and the bank identification number. Thus, the terminal does not require large storage capacity but only needs to be provided with one secure master key.

- Further objects and advantages of the subject invention will become apparent from the following detailed description taken in conjunction with the , drawings in which:

-

- Figure 1 is a diagram of a typical electronic funds transfer system in an intercharge network.

- Figure 2 is a composite flow chart illustrating the steps to implement the general concept of the key management system of the subject invention.

- Figure 3 is a composite flow chart illustrating the steps necessary to implement a key management system for use with an anticounterfeiting technique.

- Figure 4 is a composite flow chart, similar to Figure 3, including another embodiment of an anticounterfeiting technique.

- Figure 5 is a composite flow chart illustrating the key management system of the subject invention for use with the distribution of personal identification numbers (PIN's).

- Figure 6 is a composite flow chart of the key management system of the subject invention showing another embodiment for use in conjunction with the distribution of PIN's.

- Referring to Figure 1, there is shown a typical configuration for an electronics funds transfer system. More specifically, a

central host 20 is shown which acts as a network switch, routing information between a plurality oftransaction terminals 22 and issuinginstitutions 24. The issuing institutions can be banks or other service organizations which distribute transaction cards, such as credit cards or debit cards. These cards may be used at various merchants or institutions to purchase goods or services or to obtain cash. - ol Each merchant is provided with one or

more terminals 22. As shown at 22A, a terminal typically includes a reader for receiving information encoded on the magnetic stripe of the card. In addition, the terminal may include a PIN pad to permit a customer to enter their personal identification number (PIN). In accordance with the subject invention, the terminal will also include an encryption apparatus which may be provided in the main portion of the terminal or separately in the PIN pad. The location of the encryption apparatus will depend on the particular technique being selected. - Each of the terminals is connected to the host along communication lines 30. The host is also connected to the issuers along communications lines 32. In many transactions, information about the card holder and the purchase are transmitted from the terminal, along

communication lines 30, to the host. Frequently, the central host will make the approval or denial decision. In other cases, the information is routed alonglines 32, to the institution which issued the card. The authorization decision made by the institution is retransmitted to the merchant along the same communication lines. - As can be appreciated, as the use of bank cards increases in scope and geographical area, these communication costs will escalate. Therefore, it is desirable to provide some form of security through off-line analysis. In the subject specification, the term off-line is defined to mean operations which can be performed at the terminal without any communication to the host. These objectives are achieved with the key management system of the subject invention.

- Referring now to Figure 2, the general key management system of the subject invention is illustrated. This approach can be utilized to provide both an off-line anticounterfeit check and PIN verification. The flow chart is broken into three segments where Figure 2A shows the operations performed at the central host, Figure 2B shows the operations performed by the issuer and Figure 2C shows the actions taken at the terminal.

- Referring to Figure 2A, the central host or

control 20 initially generates asystem master key 40. This master key is supplied to all of theterminals 42. Since the security of the master key is of utmost importance, this distribution should be handled in a highly secure manner. There have been a number of approaches designed in the prior art for distributing keys to terminals in a secure manner. In one approach, the terminals are physically connected to the host permitting initial loading of the master key. After this time, the terminals are kept under high security until they are installed at merchant locations. In another approach, a key loading device is connected to the host and has the master key loaded therein. The key loading device is then brought to each terminal and physically connected to load the key. In either approach, the terminal should be designed such that any tampering will erase or otherwise destroy the master key, such that it can never be extracted from the terminal. - The host then generates a plurality of

secondary keys 44. These secondary keys are derived utilizing the bank identification number (BIN). As pointed out above, each institution is generally associated with an unique identification number. This identification number is encrypted using the master key. The resulting secondary keys are then distributed to the associated issuers. Again, a number of methods can be used to distribute the keys. Typically, secure encrypted communication lines are already established between the issuers and the host and therefore it is possible to transmit these keys over communication 'lines. The key may also be physically delivered using a key loading device as discussed above. - Referring to Figure 2B, the issuer is now capable of generating transaction cards. Initially, the issuer will place its BIN number on each

card 50. Typically, this information is placed on the card by encoding the information on a magnetic stripe. While this approach is fairly common, there many other ways of encoding data on the cards, all of which are within the scope of the subject invention. - The issuer will then generate

authorizaton information 52. As discussed below, this authorization information can be anticounterfeiting digits, PIN information or any other suitable identifier. The authorization information is then encrypted, using the secondary key supplied by thehost 54. The encrypted authorization information is then placed on thecard 56 in the manner described above. - The card can now be authorized in an off-line manner at the terminals. Referring to Figure 2C, the card is initially read by the terminal at 60. The terminal will typically have a card reader capable of deciphering the encoded information on the magnetic stripe. As can be appreciated, if the information is placed on the card in another manner, the terminal should have compatible reading equipment. The information which is read includes the BIN number of the institution, as well as the encrypted authorization information.

- In accordance with the subject invention, the terminal will then derive the secondary key, utilizing the master key stored at the terminal to encrypt the BIN number of the

institution 62. Once the secondary key has been derived, it can be used to analyze encrypted authorization information on thecard 64. - Since the encrypted information had been originally encrypted under the secondary key, the analysis can be handled in a number of ways. The particular approach will depend on the system design and a few examples will be discussed in detail hereinbelow. When the information is compared, if similarity is detected, the transaction can be authorized. If the information does not match, the transaction can be denied.

- Referring now to Figure 3, a more specific approach is shown for use in an anticounterfeiting scheme. Figure 3A illustrates the actions taken at the issuer, while Figure 3B describes the events at the terminal. In Figures 3 through 6, the activities of the central host are identical with those described in, Figure 2 and will not be further discussed.

- In applicant's anticounterfeiting technique, the issuer will again place the BIN number on the

card 70. The issuer will also generate a personal account number (PAN) which is unique for each card. This account number or (PAN) is placed on thecard 72. The issuer will then encrypt the PAN with thesecondary key 74. The result of this encryption is placed on thecard 76. While the above discussion is limited to the use of a PAN, this number may be combined with any other information normally on the card, such as the card expiration date. Further, the entire encrypted information need not be placed on the card but only a subset thereof. By choosing only a specific subset, the information which must fit on the card can be economized. - Referring to Figure 3B, the card will be read at the terminal 80. Thus, both the BIN number and the encrypted PAN information will be received. The terminal will then derive the secondary key, utilizing the master key to encrypt the

BIN 82. The secondary key is then used to encrypt the account number placed on the card at 84. The result of this encryption (or at least a portion thereof) can then be compared with the encrypted account information on the card. If these match, the transaction can be authorized. - Referring now to Figure 4, a more sophisticated anticounterfeiting approach is shown. More specifically, in the prior art, there have been developed various secure card properties. One such property is a Watermark, manufactured by Malco Plastics. Similar in concept to water marks found on paper currency, an electronic signature can be deeply embedded in the magnetic stripe of a card. This hidden number is very difficult for counterfeiters to reproduce. Other techniques include the precise measurement of certain physical card characteristics. These technologies can be combined with the subject system to provide even further enhancement to the card.

- Referring specifically to Figure 4A, the issuer will again place the BIN on the

card 90. The PAN is also placed on thecard 92. In addition, the secure card property, such as the Watermark is placed on the card. Because of the manufacturing sophistication necessary to implant a secure property, this step will typically be initially handled by an entity other than the issuer. The cards with the secured property placed thereon will then be supplied to the issuer. Thus, it is not intended that the order of the placement of the information on the card restrict the scope of the subject invention. The secure property, which would provide some form of numeric information, is then combined with the account number and encrypted, using asecondary key 96. The result of this encryption is then encoded on thecard 98. - Referring to Figure 4B, the information on the card, including the secure property, is read by the

terminal 100. The secondary key is derived, utilizing the master key to encrypt theBIN 102. The PAN and secure property are combined and are encrypted using thesecondary key 104. The result of this encryption is then compared with the encrypted information encoded on thecard 106. As in the previous cases, if the information matches, the transaction can be approved. However, if the information does not match, the transaction can be denied. - Referring now to Figure 5, the use of the key management system .is illustrated for use with information particularly associated with the card holder, such as a PIN. The identical system can be used for any other information associated with a specific card holder, such as dynamic signature analysis information. In the .latter case, the handwriting analysis information, unique to the cardholder, would be encoded in numeric form and encrypted, using the proper key. For simplicity, the remainder of discussion of Figures 5 and 6 will be restricted to the use of PIN's.

- Referring specifically to Figure 5A, the issuer will once again place its BIN number on the

card 110. A PIN will then be generated to be associated with the customer. Frequently, the bank generates this PIN. The PIN may also be supplied to the issuer by the cardholder. The particular approach taken can be left to the discretion of the issuing institution as there are various advantages and disadvantages with both techniques. The benefits of each technique is discussed in detail in a bulletin by the American National Standards Committee (ANSI) publication on Pin Management and Security, ANSI-X9.8 (1982). If the PIN has been generated by the institution, it must be supplied to the cardholder. - The PIN which has been selected is then encrypted using the

secondary key 114. The result of this "encryption is then placed on thecard 116. As pointed out above, this system is probably best utilized using only a partial PIN value. For example, where four digits constitute the PIN, only two digits are encrypted and placed on the card. The remaining two digits are utilized for higher value, on-line authorization. The partial PIN digits may also be derived using the full PIN. All or only a portion of these derived digits may be placed on the card. The details of implementing a partial PIN system are-known in the prior art and need not be discussed in detail. - Referring to Figure 5B, the card to be used is read by the

terminal 120. As in all cases, the secondary key is derived by encrypting the BIN utilizing the master key stored at the terminal 122. The card holder will then enter his PIN. The PIN may be entered through the PIN pad of the terminal 124. The secondary key is then utilized to compare the encrypted PIN information on the card with the PIN entered by thecard holder 126. This comparison may be carried out either by encrypting the PIN entered by the card holder or by decrypting the encrypted PIN on the card such that both PINs are in clear text. - The approach laid out in Figure 5 may be used to handle PIN information. Most encryption systems being implemented today utilize the Data encryption standard (DES), approved by the National Bureau of Standards. In this system, 64 bits of information are encrypted to generate 64 bits of enciphered output. If any of these bits are removed, decryption cannot take place. Because of the storage capacity of the magnetic stripe on a transaction card, it is often desirable to minimize the amount of information which needs to be encoded. A variety of techniques have been developed to achieve this result. One of the approaches is known generally as PIN offset generation. The latter approach is indicated in Figure 6 and requires less information to be encoded on the card.

- Referring specifically to Figure 6A, the issuer places the BIN number on the

card 130. In addition, the PAN is placed on thecard 132. A PIN is generated 134 in a manner described above. In this embodiment, rather than encrypting the PIN, the PAN is encrypted 136. The resulting encryption is then combined with the PIN to define acoded value 138. There are a number of ways to combine the encrypted PAN with the PIN. In the preferred embodiment, a portion of the encrypted PAN is added to the PIN using a modulo 10 procedure. Other more sophisticated approaches may be taken. In any case, the coded value is then placed on thecard 140. - Referring to Figure 6B, at the initiation of the transaction, the card is read at the terminal 150. The PIN is received from the

cardholder 152. The secondary key is then derived utilizing the master key to encrypt theBIN 154. The PAN is then encrypted under thesecondary key 156. The encrypted PAN is then compared with the information placed on the card. This can conveniently be done in two ways, as shown at 158 and 160. More specifically, the encrypted PAN (or a portion thereof) is combined with the coded value and then compared with the PIN entered by the card holder. Where the original combination at 138 was by addition, the encrypted PAN is subtracted from the coded value, which should yield the PIN. Another alternative (160) is to combine the newly encrypted PAN (or a portion thereof) with the PIN entered by the card holder. This result should generate the coded value which has been placed on the card. In either case, if the comparison matches, the transaction can be authorized. - In summary, there has been provided a new and improved key management system, for use in an EFT environment, which permits off-line authorization of a transaction card. In the subject system, a central host generates a master key which is then supplied to all the terminals in the system. The host then derives a secondary key for each issuing institution by encrypting the BIN number of the issuing institution under the master key. The secondary keys are then supplied to the issuing institution.

- When the institution issues a card, it places its BIN number on the card. In addition, authorization information is placed on the card in encrypted form. This information is encrypted under the secondary key associated with the institution. This information may include anticounterfeiting digits or PIN information. At the terminal, the information on the card is read. The terminal then derives the secondary key, utilizing the master key stored at the terminal to encrypt the BIN of the institution. The secondary key is then used to permit analysis of the encrypted authorization information which has been placed on the card. By this arrangement, off-line authorization can be carried out to enhance the security of the transaction card network. Furthermore, each of the issuing institutions is given a different cryptographic key, thereby further enhancing overall system security.

- The disclosure has included a description of a number of different security approaches which can utilize the subject key management system. These techniques can be used alone or in combination. If used in combination, it could be beneficial to have the issuing institutions use a different secondary key for each technique. This could be accomplished in a number of ways. For example, a different master key could be generated for each technique, or the BIN could be modified in a set way before it is encrypted.

- While the subject invention has been described with reference to a preferred embodiment, it should be understood that various other changes and modifications could be made therein, by one skilled in the art, without varying from the scope and spirit of the subject invention as defined by the appended claims.

Claims (17)

Applications Claiming Priority (2)

| Application Number | Priority Date | Filing Date | Title |

|---|---|---|---|

| US52916183A | 1983-09-02 | 1983-09-02 | |

| US529161 | 1995-09-13 |

Publications (3)

| Publication Number | Publication Date |

|---|---|

| EP0138320A2 true EP0138320A2 (en) | 1985-04-24 |

| EP0138320A3 EP0138320A3 (en) | 1986-02-19 |

| EP0138320B1 EP0138320B1 (en) | 1989-03-15 |

Family

ID=24108779

Family Applications (1)

| Application Number | Title | Priority Date | Filing Date |

|---|---|---|---|

| EP19840305480 Expired EP0138320B1 (en) | 1983-09-02 | 1984-08-10 | Cryptographic key management system |

Country Status (3)

| Country | Link |

|---|---|

| EP (1) | EP0138320B1 (en) |

| JP (1) | JPS6061863A (en) |

| DE (1) | DE3477331D1 (en) |

Cited By (16)

| Publication number | Priority date | Publication date | Assignee | Title |

|---|---|---|---|---|

| EP0237815A2 (en) * | 1986-02-18 | 1987-09-23 | RMH Systems, Inc. | Off line cash card system and method |

| FR2600190A1 (en) * | 1986-06-16 | 1987-12-18 | Bull Cp8 | Method for diversifying a basic key and for authenticating a key thus diversified as having been derived from a predetermined basic key, and system for implementation |

| EP0281057A2 (en) * | 1987-03-04 | 1988-09-07 | Siemens Nixdorf Informationssysteme Aktiengesellschaft | Circuitry for securing the access to a data processor by means of an IC card |

| EP0588339A2 (en) * | 1992-09-18 | 1994-03-23 | Nippon Telegraph And Telephone Corporation | Method and apparatus for settlement of accounts by IC cards |

| FR2697361A1 (en) * | 1992-10-27 | 1994-04-29 | Bull Cp8 | Method and system for recording information on a medium making it possible to subsequently certify the originality of this information. |

| WO1995030976A1 (en) * | 1994-05-10 | 1995-11-16 | Cp8 Transac | Method for the production of a key common to two devices for implementing a common cryptographic procedure and associated apparatus |

| US5796835A (en) * | 1992-10-27 | 1998-08-18 | Bull Cp8 | Method and system for writing information in a data carrier making it possible to later certify the originality of this information |

| WO1998059327A1 (en) * | 1997-06-10 | 1998-12-30 | Digital Equipment Bcfi Ab | Safety module |

| WO2001037478A2 (en) * | 1999-11-19 | 2001-05-25 | Storage Technology Corporation | Encryption key management system using multiple smart cards |

| FR2829332A1 (en) * | 1986-04-30 | 2003-03-07 | Thomson Csf | Key management system has secondary key encrypted subscriber key distribution |

| EP1443440A1 (en) * | 2001-11-02 | 2004-08-04 | Sony Corporation | Electronic transaction system |

| US7110986B1 (en) * | 2001-04-23 | 2006-09-19 | Diebold, Incorporated | Automated banking machine system and method |

| US7328337B2 (en) | 2001-05-25 | 2008-02-05 | America Online, Incorporated | Trust grant and revocation from a master key to secondary keys |

| US8019084B1 (en) | 2001-04-23 | 2011-09-13 | Diebold, Incorporated | Automated banking machine remote key load system and method |

| US20140279559A1 (en) * | 2013-03-15 | 2014-09-18 | Mastercard International Incorporated | System and method for using multiple payment accounts using a single payment device |

| EP2558997A4 (en) * | 2010-04-13 | 2016-01-20 | Mastercard International Inc | Method and apparatus for global replacement card services |

Citations (3)

| Publication number | Priority date | Publication date | Assignee | Title |

|---|---|---|---|---|

| EP0003756A2 (en) * | 1978-03-01 | 1979-09-05 | International Business Machines Corporation | Transaction execution system |

| WO1981002655A1 (en) * | 1980-03-10 | 1981-09-17 | M Sendrow | A system for authenticating users and devices in on-line transaction networks |

| EP0068805A1 (en) * | 1981-06-26 | 1983-01-05 | VISA U.S.A. Inc. | End-to-end encryption system and method of operation |

-

1984

- 1984-08-10 EP EP19840305480 patent/EP0138320B1/en not_active Expired

- 1984-08-10 DE DE8484305480T patent/DE3477331D1/en not_active Expired

- 1984-08-10 JP JP59168734A patent/JPS6061863A/en active Pending

Patent Citations (3)

| Publication number | Priority date | Publication date | Assignee | Title |

|---|---|---|---|---|

| EP0003756A2 (en) * | 1978-03-01 | 1979-09-05 | International Business Machines Corporation | Transaction execution system |

| WO1981002655A1 (en) * | 1980-03-10 | 1981-09-17 | M Sendrow | A system for authenticating users and devices in on-line transaction networks |

| EP0068805A1 (en) * | 1981-06-26 | 1983-01-05 | VISA U.S.A. Inc. | End-to-end encryption system and method of operation |

Cited By (34)

| Publication number | Priority date | Publication date | Assignee | Title |

|---|---|---|---|---|

| EP0237815A3 (en) * | 1986-02-18 | 1989-08-02 | Rmh Systems, Inc. | Off line cash card system and method |

| EP0237815A2 (en) * | 1986-02-18 | 1987-09-23 | RMH Systems, Inc. | Off line cash card system and method |

| FR2829332A1 (en) * | 1986-04-30 | 2003-03-07 | Thomson Csf | Key management system has secondary key encrypted subscriber key distribution |

| FR2600190A1 (en) * | 1986-06-16 | 1987-12-18 | Bull Cp8 | Method for diversifying a basic key and for authenticating a key thus diversified as having been derived from a predetermined basic key, and system for implementation |

| EP0281057A2 (en) * | 1987-03-04 | 1988-09-07 | Siemens Nixdorf Informationssysteme Aktiengesellschaft | Circuitry for securing the access to a data processor by means of an IC card |

| EP0281057A3 (en) * | 1987-03-04 | 1990-04-18 | Siemens Aktiengesellschaft | Circuitry for securing the access to a data processor by means of an ic card |

| EP0588339A2 (en) * | 1992-09-18 | 1994-03-23 | Nippon Telegraph And Telephone Corporation | Method and apparatus for settlement of accounts by IC cards |

| EP0588339A3 (en) * | 1992-09-18 | 1995-05-24 | Nippon Telegraph & Telephone | Method and apparatus for settlement of accounts by IC cards. |

| WO1994010660A1 (en) * | 1992-10-27 | 1994-05-11 | Bull Cp8 | Method and system for writing data onto a medium so as to enable subsequent verification of authenticity |

| EP0595720A1 (en) * | 1992-10-27 | 1994-05-04 | Bull Cp8 | Process and system for recording information on a data carrier enabling to later certify the originality of this information |

| US5796835A (en) * | 1992-10-27 | 1998-08-18 | Bull Cp8 | Method and system for writing information in a data carrier making it possible to later certify the originality of this information |

| FR2697361A1 (en) * | 1992-10-27 | 1994-04-29 | Bull Cp8 | Method and system for recording information on a medium making it possible to subsequently certify the originality of this information. |

| WO1995030976A1 (en) * | 1994-05-10 | 1995-11-16 | Cp8 Transac | Method for the production of a key common to two devices for implementing a common cryptographic procedure and associated apparatus |

| FR2719925A1 (en) * | 1994-05-10 | 1995-11-17 | Bull Cp8 | Method for producing a common key in two devices for implementing a common cryptographic procedure, and associated apparatus. |

| US5729609A (en) * | 1994-05-10 | 1998-03-17 | Cp8 Transac | Method for producing a common key in two devices, in order to implement a common cryptographic procedure, and associated apparatus |

| AU692876B2 (en) * | 1994-05-10 | 1998-06-18 | Banksys S.A. | Method for the production of a key common to two devices for implementing a common cryptographic procedure and associated apparatus |

| WO1998059327A1 (en) * | 1997-06-10 | 1998-12-30 | Digital Equipment Bcfi Ab | Safety module |

| WO2001037478A2 (en) * | 1999-11-19 | 2001-05-25 | Storage Technology Corporation | Encryption key management system using multiple smart cards |

| US6831982B1 (en) | 1999-11-19 | 2004-12-14 | Storage Technology Corporation | Encryption key management system using multiple smart cards |

| WO2001037478A3 (en) * | 1999-11-19 | 2002-01-10 | Storage Technology Corp | Encryption key management system using multiple smart cards |

| US8090663B1 (en) | 2001-04-23 | 2012-01-03 | Diebold, Incorporated | Automated banking machine system and method |

| US8019084B1 (en) | 2001-04-23 | 2011-09-13 | Diebold, Incorporated | Automated banking machine remote key load system and method |

| US7110986B1 (en) * | 2001-04-23 | 2006-09-19 | Diebold, Incorporated | Automated banking machine system and method |

| US8181018B2 (en) | 2001-05-25 | 2012-05-15 | Aol Inc. | Master key trust grants and revocations for minor keys |

| US7328337B2 (en) | 2001-05-25 | 2008-02-05 | America Online, Incorporated | Trust grant and revocation from a master key to secondary keys |

| US8683198B2 (en) | 2001-05-25 | 2014-03-25 | Facebook, Inc. | Master key trust grants and revocations for minor keys |

| CN1327361C (en) * | 2001-11-02 | 2007-07-18 | 索尼公司 | Electronic transaction system |

| EP1443440A1 (en) * | 2001-11-02 | 2004-08-04 | Sony Corporation | Electronic transaction system |

| EP1443440A4 (en) * | 2001-11-02 | 2004-12-08 | Sony Corp | Electronic transaction system |

| EP2558997A4 (en) * | 2010-04-13 | 2016-01-20 | Mastercard International Inc | Method and apparatus for global replacement card services |

| US20140279559A1 (en) * | 2013-03-15 | 2014-09-18 | Mastercard International Incorporated | System and method for using multiple payment accounts using a single payment device |

| JP2016514328A (en) * | 2013-03-15 | 2016-05-19 | マスターカード インターナショナル インコーポレーテッド | Method and system for using multiple payment accounts using one payment device |

| AU2014237800B2 (en) * | 2013-03-15 | 2017-07-20 | Mastercard International Incorporated | System and method for using multiple payment accounts using a single payment device |

| US9947001B2 (en) * | 2013-03-15 | 2018-04-17 | Mastercard International Incorporated | System and method for using multiple payment accounts using a single payment device |

Also Published As

| Publication number | Publication date |

|---|---|

| JPS6061863A (en) | 1985-04-09 |

| EP0138320B1 (en) | 1989-03-15 |

| EP0138320A3 (en) | 1986-02-19 |

| DE3477331D1 (en) | 1989-04-20 |

Similar Documents

| Publication | Publication Date | Title |

|---|---|---|

| EP0385400B1 (en) | Multilevel security apparatus and method with personal key | |

| US4357529A (en) | Multilevel security apparatus and method | |

| US6816058B2 (en) | Bio-metric smart card, bio-metric smart card reader and method of use | |

| US7818812B2 (en) | Article and system for decentralized creation, distribution, verification and transfer of valuable documents | |

| US4328414A (en) | Multilevel security apparatus and method | |

| US4386266A (en) | Method for operating a transaction execution system having improved verification of personal identification | |

| EP0047285B1 (en) | A system for authenticating users and devices in on-line transaction networks | |

| CA1162306A (en) | Multilevel security apparatus and method | |

| US7177835B1 (en) | Method and device for generating a single-use financial account number | |

| US6163771A (en) | Method and device for generating a single-use financial account number | |

| EP0138320B1 (en) | Cryptographic key management system | |

| JPH0334641A (en) | Method of encrypting transmission data using special key | |

| EP0981807A2 (en) | Integrated circuit card with application history list | |

| WO1997010560A1 (en) | Stored value transaction system and method using anonymous account numbers | |

| EP1125181A2 (en) | Apparatus for and method of electronic currency generation, transfer and redemption | |

| Caelli et al. | Financial and Banking Networks | |

| AU2002308486A1 (en) | A bio-metric smart card, bio-metric smart card reader, and method of use | |

| MXPA01001407A (en) | Apparatus for and method of electronic currency generation, transfer and redemption |

Legal Events

| Date | Code | Title | Description |

|---|---|---|---|

| PUAI | Public reference made under article 153(3) epc to a published international application that has entered the european phase |

Free format text: ORIGINAL CODE: 0009012 |

|

| AK | Designated contracting states |

Designated state(s): DE FR GB SE |

|

| PUAL | Search report despatched |

Free format text: ORIGINAL CODE: 0009013 |

|

| AK | Designated contracting states |

Designated state(s): DE FR GB SE |

|

| 17P | Request for examination filed |

Effective date: 19860731 |

|

| 17Q | First examination report despatched |

Effective date: 19870814 |

|

| GRAA | (expected) grant |

Free format text: ORIGINAL CODE: 0009210 |

|

| AK | Designated contracting states |

Kind code of ref document: B1 Designated state(s): DE FR GB SE |

|

| REF | Corresponds to: |

Ref document number: 3477331 Country of ref document: DE Date of ref document: 19890420 |

|

| ET | Fr: translation filed | ||

| PLBE | No opposition filed within time limit |

Free format text: ORIGINAL CODE: 0009261 |

|

| STAA | Information on the status of an ep patent application or granted ep patent |

Free format text: STATUS: NO OPPOSITION FILED WITHIN TIME LIMIT |

|

| 26N | No opposition filed | ||

| PGFP | Annual fee paid to national office [announced via postgrant information from national office to epo] |

Ref country code: GB Payment date: 19930729 Year of fee payment: 10 |

|

| PG25 | Lapsed in a contracting state [announced via postgrant information from national office to epo] |

Ref country code: GB Effective date: 19940810 |

|

| EAL | Se: european patent in force in sweden |

Ref document number: 84305480.0 |

|

| GBPC | Gb: european patent ceased through non-payment of renewal fee |

Effective date: 19940810 |

|

| PGFP | Annual fee paid to national office [announced via postgrant information from national office to epo] |

Ref country code: SE Payment date: 19950713 Year of fee payment: 12 |

|

| PGFP | Annual fee paid to national office [announced via postgrant information from national office to epo] |

Ref country code: FR Payment date: 19950717 Year of fee payment: 12 |

|

| PGFP | Annual fee paid to national office [announced via postgrant information from national office to epo] |

Ref country code: DE Payment date: 19950725 Year of fee payment: 12 |

|

| PG25 | Lapsed in a contracting state [announced via postgrant information from national office to epo] |

Ref country code: SE Effective date: 19960811 |

|

| PG25 | Lapsed in a contracting state [announced via postgrant information from national office to epo] |

Ref country code: FR Effective date: 19970430 |

|

| PG25 | Lapsed in a contracting state [announced via postgrant information from national office to epo] |

Ref country code: DE Effective date: 19970501 |

|

| EUG | Se: european patent has lapsed |

Ref document number: 84305480.0 |

|

| REG | Reference to a national code |

Ref country code: FR Ref legal event code: ST |